Analysis of Decentralized Perpetual Swaps

Introduction

Recently, perpetual swap protocols have sparked many discussions in DeFi, and perpetual swaps have become one of the first on-chain derivatives categories to gain meaningful trading volumes. In this report, we aim to address the following three questions about decentralized perpetual swaps as a subsector of on-chain derivatives:

- Projected total market cap of the decentralized derivatives market;

- Differences between existing DeFi derivatives protocols;

- Performances of existing perpetual swap protocols.

Projected Total Market Cap

To understand the total addressable market of on-chain derivatives, we compare spot and derivatives trading data from centralized exchange Huobi Global, top decentralized spot trading protocol Uniswap, and decentralized derivative trading protocol dYdX . Unless noted otherwise the data used in this report is from August 6, 2020 and February 1, 2021.

Since August 2020, DEXes, represented by Uniswap, have grown rapidly. Its daily trading volume climbed from 8,241 BTC on August 6, 2020 all the way to 30,062 BTC on February 1, 2021, an increase of 3.6 times. Meanwhile, CEXes, represented by Huobi Global, also experienced a 1.6 times increase in its spot trading volume.

Comparison of Huobi Spot, Huobi Derivatives, Uniswap and dYdX Trading Volumes

Source: Huobi DeFi Labs

As shown by the blue line in the chart above, in CEXes like Huobi Global, spot and derivatives trading volumes typically increase and decrease in tandem. The significant increase in Uniswap trading volume (gray solid line), on the other hand, did not correlate with dYdX’s trading volume (gray dashed line). During this period, Huobi Global spot trading volume was approximately 19% of its derivatives trading volume; conversely, Uniswap trading was at 331% of dYdX.

Market Shares of spot and derivatives trading on Huobi Global and on Decentralized Trading Protocols

Source: Huobi DeFi Labs

For a more accurate comparison between crypto derivatives to spot trading volumes, we analyze data from the top five centralized exchanges in terms of daily volumes.

Comparison of average daily spot and derivatives trading volumes on major centralized exchanges

Source: Huobi DeFi Labs

On average, the derivatives trading volume of the five centralized exchanges is 4.82x their spot trading volume. If decentralized derivatives protocols also reach this level, the average daily turnover of the decentralized derivatives trading market should be about $4.7B, based on Uniswap’s average daily trading volume (~$976M) for the past 30 days.

Of the four decentralized perpetual swap protocols currently launched, Perpetual Protocol sees the highest average daily trading volume at $29M. The total average daily volume of the four protocols is $67.7M, which is only 1.4% of the size estimated above. Thus, we believe there is space for 50x+ growth in decentralized perpetual swap protocols. Perpetual contracts are the mainstay of crypto derivatives trading, but their size in the decentralized market does not match that of spot.

Average daily volume of top perpetual swaps

Source: Huobi DeFi Labs

Analysis of Existing Perpetual Swaps Protocols

Product Comparison

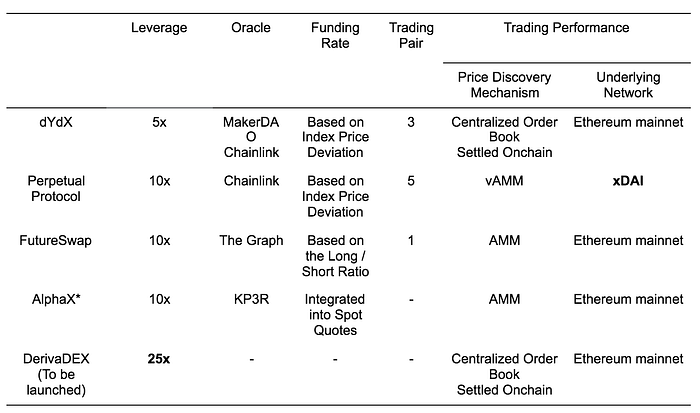

According to CoinTelegraph research*, supports for high leverage, more tokens and good trading experience are critical for users of CEXes. Among these criteria, trading experience largely depends on a protocol’s price discovery mechanism and the underlying blockchain’s efficiency. We here summarize the design of several perpetual swap protocols.

dYdX, DerivaDEX, Perpetual Protocol, FutureSwap and AlphaX are decentralized perpetual contract trading protocols that are currently live or about to go live.

Key indicators of existing decentralized derivative protocols

*AlphaX information is from the community, and the final official docs after launch shall prevail

Source: Huobi DeFi Labs

Both DerivaDEX and dYdX adopt an order-book model for price discovery, which is easier for ordinary users to understand. However, it is settled on the Ethereum mainnet and requires gas fees for deposits & withdrawals. In comparison, the pricing of the remaining three protocols is based on the constant product AMM; Perpetual Protocol’s vAMM separates pricing (constant product formula) from user deposit, so no collateral is held in the AMM liquidity pool.

Notably, DerivaDEX provides the highest leverage (25x), although it is still far from the maximum leverage of 100x on some centralized exchanges. Meanwhile, Perpetual Protocol supports the most trading pairs, including BTC, ETH, YFI, DOT and SNX to USDC. The table above shows that each of the four has its own strengths, and there is no one protocol that is superior in all aspects now.

Liquidity Comparison

In addition to protocol designs, liquidity is another important concern for derivatives traders. In this subsection, we analyze the liquidity of each decentralized perpetual swap protocol and compare them with CEXes.

dYdX’s and DerivaDEX’s order book mechanisms are similar to that of CEXes, although DerivaDEX is not yet online and its data unable to access. dYdX’s ETH pair has a total of 9.933 ETH pending orders within the $0.05 — $2,000 range, and 9,830.7 ETH (98%) pending orders on the far end of the orderbook (deviating more than 5% from the latest price). However, since perpetual swap traders place a lot of market-price orders and are mostly short-term traders*. Having most orders deviated too much from the latest price does not improve trading experience. In other words, although dYdX chooses an off-chain orderbook and on-chain settlement model to avoid high gas fees, it does not meet users’ trading needs. The orderbook depth of dYdX is shown in the figure below.

dYdX orderbook Depth (ETH-USD pair)

Time: February 2, 2021

Source: Huobi DeFi Labs

Centralized exchanges, represented by Huobi Global, have more established data infrastructure and strong market maker networks, therefore they usually have an unparalleled edge in liquidity. As shown in the chart below, Huobi ETH-USDT perpetual contract has a pending order volume of 601.55 ETH around the market price (within 5% deviation from the latest price), which is larger than dYdX’s 102.3 ETH.

Huobi Global Perpetual Orderbook (ETH-USDT pair)

Time: February 2, 2021

Source: Huobi DeFi Labs

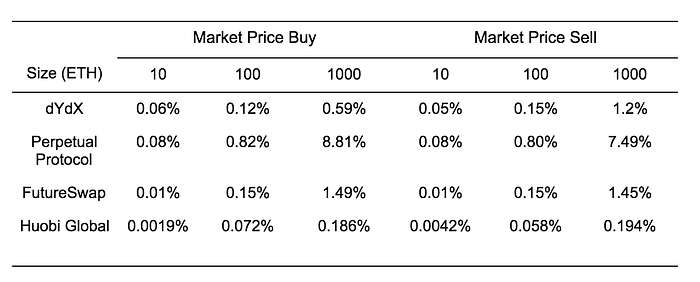

When it comes to liquidity, order book-based protocols in general provide better trading experience than their AMM counterparts, while the latter requires a sufficient number of liquidity providers (LPs) to achieve large-scale usability. Perpetual Protocol and FutureSwap use vAMMs and AMM for price discovery respectively, and both claim to provide *low slippage; liquidity mining is also able to bring more LPs to Perpetual Protocol and FutureSwap.

We performed some tests on the slippage of these protocols and the results are as follows. FutureSwap currently returns the best slippage among decentralized perpetual swap protocols, but it is still far from the performance of centralized exchanges (Huobi Global, for example).

Slippage Test Results (ETH-USDT pair)

Time: February 2, 2021

Source: Huobi DeFi Labs

Onchain Data

As shown in the chart below, dYdX has the highest 30 days peak daily trading volume among the four, while Perpetual Protocol has the highest average daily transaction count.

And based on the average daily trading volume and the average daily transaction count, FutureSwap has the largest average trade size, while Perpetual Protocol has the smallest. This may indicate that Perpetual Protocol is more suitable for retail investors. Perpetual Protocol runs on xDAI with low gas fees and offers contracts on tokens such as DOT and YFI, which can be more retail user friendly.

dYdX and FutureSwap are more attractive to professional traders and large investors who have on-chain hedging needs because of the lower slippage. However, since FutureSwap has been online for only 14 days so far, the trading volume fluctuates a lot, and more data is needed to verify this suggestion.

Although decentralized perpetual swap protocols have grown rapidly lately, the data still falls far behind that of centralized exchanges. Take Huobi Global for example, the average daily trading volume of Futures is $18.7B (644 times that of Perpetual Protocol) and the highest volume in the last 30 days reached $33.5B (265 times that of dYdX).

Trading statistics of major decentralized perpetual swap protocols

Source: Huobi DeFi Labs

Conclusion

Since the summer of 2020, DeFi has flourished on Ethereum. However, the development of perpetual swaps has significantly lagged behind that of spot trading due to its rigorous requirements for system performance and liquidity.

However, several decentralized perpetual swap protocols are gradually innovating. dYdX uses off-chain order making; Perpetual Protocol adopts a side-chain to solve the problem of network congestion; FutureSwap and Perpetual Protocol try to redefine market makers with AMM similar to Uniswap. Still, as mentioned above, the user-friendliness of current decentralized perpetual swap protocols is lacking.

The five protocols covered in this report have very different user profiles. Perpetual Protocol and FutureSwap are both running liquidity mining programs to bootstrap trading volume and liquidity pool lockups. At the same time, Perpetual Protocol is built on the xDAI sidechain where gas fees are low, which in turn helps it attract more transactions. dYdX’s centralized order book avoids gas consumption completely and may attract more large traders to hedge their on-chain positions.

Based on the research in this report, decentralized perpetual swaps are currently limited by their lack of liquidity and network efficiency, and are therefore not applicable to many traders. Specifically, in terms of liquidity, order book trading protocols require a large amount of market maker resources, while AMM mechanism protocols need to control the balance between liquidity mining and project development (a relatively aggressive liquidity mining plan can significantly improve liquidity in the short term, but is not conducive to long-term project development); as for network efficiency, the increasing gas fee of the Ethereum mainnet will limit trading operations, and various Layer 2 solutions will lessen inter-protocol combinability. Therefore, we believe:

- The combination of Layer 2 (including sidechain, Roll-up) and off-chain order book or AMM may bring new possibilities to this sector

- A relatively aggressive liquidity mining program may be able to bring the protocol sufficient liquidity to meet trading demand in the short term

- A more accurate calculation of index prices (or better oracles) will dramatically improve user experience and avoid unnecessary liquidation that causes heavy losses to traders

- perpetual swaps has high requirements for timeliness and technical indicators, and a professional UI will also be the focus of projects in this category

* https://cointelegraph.com/explained/derivatives-in-crypto-explained

** https://docs.perp.fi/getting-started/how-it-works